By Marshall Henry, Bureau of the Fiscal Service.

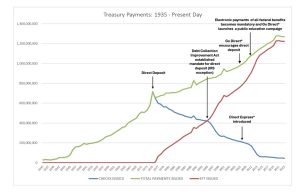

In 1975, the U.S. Treasury issued over 700 million paper checks to federal beneficiaries. These checks were printed in-house and mailed to recipients via the U.S. Postal Service. This was the most efficient distribution method, up to that point, but that same year, the first electronic payment was made through what is now called automated clearing house (ACH), or direct deposit. This changed the payment landscape forever. Soon thereafter, legislation mandated electronic payments for most federal payments and Treasury launched its “Go Direct®” public education campaign, encouraging direct deposit.

In 2008, the Direct Express® prepaid debit card was introduced to deliver electronic payments to unbanked individuals who could not receive funds via direct deposit. Most recently, in March 2025, the president signed an Executive Order (EO 14247: Modernizing Payments To and From America’s Bank Account) mandating the transition to electronic payments for all federal disbursements, further strengthening the electronic payment trend in federal government.

The undeniable rise of electronic payments has already, over the past several decades, precipitated operational improvements and cost savings for the American taxpayer. The continued phasing out of paper checks is accelerating the government toward an efficient and effective payments landscape that Treasury officials of the mid-seventies could have hardly imagined.

Efficiency Gains

By leveraging electronic payments, Treasury has streamlined its distribution of benefit payments—delivering the exceptional service beneficiaries rely on, while saving taxpayers money. Paper checks are inconvenient and costly (both to issue and to cash), and carry a heightened risk of loss, fraud, and theft. Historically, Treasury checks are 16 times more likely than an electronic funds transfer to be reported lost or stolen, returned undeliverable, or otherwise altered. The Direct Express® card, on the other hand, offers enhanced security features that mitigate these risks—and, by extension, the time and money that must be spent resolving them. For example, Direct Express® cards can be added to smartphone mobile wallets for use with Apple or Google Pay. Mobile wallets protect the actual card number, using a unique digital number instead. This feature allows cardholders to make payments from their phone, so they can even choose to leave their physical card safe at home if they wish. Also, each Direct Express® card is protected by a Personal Identification Number (PIN) and employs EMV (Chip and Pin) technology, ensuring that only the authorized recipient can access the funds.

Additionally, Direct Express® cards are protected by Regulation E, a federal regulation that safeguards cardholders from unauthorized use and provides guidelines for financial institutions. This protection includes consumer protections against unauthorized use of the card, as well as FDIC insurance for funds deposited on the card.

Fig 1. Benefit Checks and EFT Timeline

Fig 1. Benefit Checks and EFT Timeline

Fig 1. Benefit Checks and EFT Timeline

Fig 1. Benefit Checks and EFT TimelineThese efficiency improvements represent Treasury’s commitment to serving as a good steward of taxpayer dollars. By transitioning to the Direct Express® card, the U.S. government significantly reduced administrative expenses, and the operational costs associated with printing, mailing, and processing paper checks by an estimated $120 million annually. Funds that were previously allocated to check production and distribution have been redirected to other critical areas, enhancing the overall efficiency of government operations. Moreover, the program minimizes the need for the physical infrastructure and personnel required for handling paper checks.

Effective Delivery

In addition to the cost savings associated with efficiency, the Direct Express® card program prioritizes effectiveness.Benefit recipients can immediately access funds once added to their card, enabling them to meet their financial obligations promptly. This timeliness is particularly crucial for beneficiaries who rely on these funds for essential expenses, such as rent, utilities, and healthcare. Furthermore, the accessibility of the program likely reduces the potential for unclaimed benefits, as we can surmise that recipients are more likely to access and use their funds when they are readily available on a prepaid card. Finally, Direct Express® keeps detailed transaction records for each cardholder. These records give a clear and comprehensive overview of how funds are spent and can be used by cardholders to manage and review transactions for potentially fraudulent charges.

Treasury can benefit from this data as well. Sensitive cardholder transactional data is protected by industry-standard privacy controls, but Treasury gleans insights broader card adoption and usage trends. This fosters accountability, allowing Treasury to swiftly identify and address any discrepancies or irregularities in benefit disbursements. Transaction records also facilitate audits and evaluations, ensuring both that the program delivers on its mission and that federal funds are spent in accordance with program guidelines.

Conclusion

In conclusion, we believe that the Direct Express® card program exemplifies Treasury’s commitment to delivering a modern payment experience for all. In step with industry, the federal government is phasing out its use of paper checks in favor of electronic solutions that represent a more efficient use of taxpayers’ time and money. Furthermore, just as customers of any financial institution would expect, Direct Express® conducts real-time, responsive monitoring and offers proactive safeguards that keep cardholders’ information and money safe. These features ensure that program funds are being disbursed and spent effectively. We look forward to realizing the next steps in our all-electronic vision, and chronicling the gains associated with each milestone along the way.

SOURCE: Fiscal Service

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}